On the Cover of Photonics Research, Volume 10, 2023:

Recommendation: In the field of financial derivatives pricing, accurate and efficient computational methods are crucial. However, traditional option pricing models face great challenges in dealing with the increasing complexity of financial markets. Photonics computing chips, known for their high speed and low energy consumption, have attracted great attention. At the same time, quantum amplitude amplification algorithms provide the potential for quadratic speedup in option pricing. A collaborative research team from Hong Kong Polytechnic University and the National University of Singapore designed an efficient photonic computing chip dedicated to option pricing. The chip employs a unary option pricing algorithm, reducing the complexity of the photonic circuit compared to conventional binary algorithms, thus accelerating option pricing. The utilization of generative adversarial networks facilitates efficient learning and loading of asset distributions, accurately capturing market trends. This photonic computing chip offers the financial industry a rapid and accurate solution for option pricing, introducing new computational tools and opening new prospects for the commercial application of photonics computing technology.

——Beibei Li,Asisstant Editor of Photonics Research

In the field of financial derivatives pricing, precise and efficient computational methods are the focus of attention for financial institutions and investors. Options, a typical financial derivative, allow the holder to buy or sell a certain quantity of assets at a predetermined price (i.e., the strike price) before a specified expiration date. The option pricing largely depends on the random evolution of asset prices. Traditional option pricing models such as the Black-Scholes-Merton (BSM) model face increasing challenges due to the oversimplification of market dynamics in the face of growing financial market complexity. The increase in market volatility, non-linear characteristics, and randomness makes it difficult for traditional models to capture the true value of financial derivatives. Additionally, traditional numerical methods like Monte Carlo simulations require substantial computational resources, limiting their application in financial transactions. Reducing the computational resources required by the model and speeding up the option pricing process is crucial for the financial industry.

In this context, photonic computing chips, with their high speed and low energy costs, have been driving research in the fields of machine learning and high-performance computing. Simultaneously, researchers have started exploring the potential of quantum algorithms in financial computation problems. They suggest that quantum amplitude amplification algorithms could achieve quadratic speedup in option pricing, providing more efficient services to the financial industry. However, current quantum option algorithms rely mainly on binary algorithms and superconducting devices. This approach requires complex and dense chip connections and demands a high fidelity of gate operations, making practical application challenging in the absence of a universal quantum computer. Moreover, superconducting devices require large, energy-consuming, and expensive peripheral equipment such as cooling systems, making them less optimistic for large-scale industrial applications.

To solve these problems, Professor Ai Qun Liu's research group at Hong Kong Polytechnic University and Professors José Ignacio Latorre and Leong Chuan Kwek at the National University of Singapore Quantum Technology Center collaborated to design an efficient photonic computing chip dedicated to option pricing. The research team proposed a unary option pricing algorithm that integrates quantum amplitude amplification, designed and manufactured the corresponding photonic computing chip, and achieved rapid and accurate calculation of option pricing. The chip exhibits advantages such as a streamlined hardware structure, high-speed information transmission, low energy consumption, and strong stability, marking a significant step in the development of dedicated photonic processors and potentially improving the efficiency and quality of financial services. The research findings were published in the 10th issue of Photonics Research in 2003.

Compared to conventional binary algorithms, the unary algorithm structure is more efficient, by simplifying the depth of photonic circuits and transforming the required non-local controlled gates into linear calculations through the expansion of Hilbert space, without relying on universal quantum computing devices. In the design of the photonic computing chip, the research team divided the functional modules into key components such as asset price distribution loading, expected payoff calculation, and quantum amplitude estimation algorithms. By designing the corresponding waveguide structures and assembling them one by one, the team completed the entire algorithm's functionality. In the asset price distribution loading module, the team introduced generative adversarial networks, achieving efficient learning and loading of asset distributions, and accurately capturing market trends.

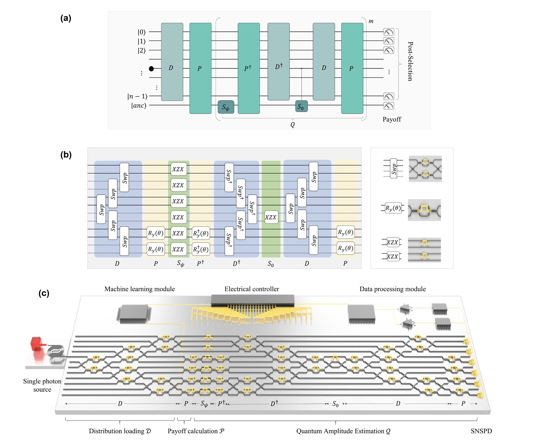

Figure 1(a) shows the algorithmic model of unary option pricing, including three modules: distribution loading module , payoff calculation module , and quantum amplitude estimation module Q of each asset price, which aims to achieve quadratic speedup at the target precision. Figure 1(b) illustrates the optical circuit model, where each module of the unary algorithm is mapped to a linear optical operator. The unary basis of dimensions is achieved by encoding a single photon in different waveguides using path encoding. Payoff calculation requires an ancilla qubit to store the expected payoff for each asset price, thus extending the algorithm's Hilbert space to -dimensional. To avoid non-local controlled gates in the implementation of the photonic chip, an ancilla waveguide is added to each unary waveguide mode, representing the effect of the ancilla qubit. Therefore, each element of the unary basis is represented by two waveguides, and controlled operations in the original algorithm are transformed into linear operations in the optical circuit. Figure 1(c) shows the detailed chip design of the photonic processor architecture, where each linear optical operator is replaced by the corresponding waveguide structure. The entire chip can be programmed and configured through the integrated thermos-optic phase shifter.

Figure 1 Photonic chip design of the unary option pricing algorithm. (a) Algorithmic model for unary option pricing. The input state consists of -dimensional quantum bits and 2D ancilla bits. It includes the following modules: , distribution loading; , payoff calculation; , quantum amplitude amplification. Module obtains the expected payoff by measuring the ancilla bits. (b) Optical circuit model. The algorithm model is transformed into linear optical operators. Each element of the unary basis is represented by two waveguides, extending the -dimensional unary basis to a 2-dimensional Hilbert space. The relevant linear optical operators have their waveguide structures. (c) Design and architecture of the photonic chip. By converting the optical circuit model into waveguide structures, distribution loading, payoff calculation, and amplitude estimation are implemented sequentially. Distribution loading is trained using generative adversarial networks embedded in the machine learning module.

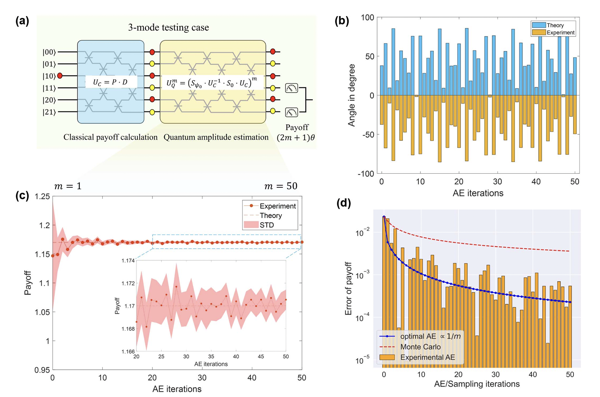

Using the fabricated photonic computing chip, the research team demonstrates an option pricing problem with three asset values as a proof of concept. As shown in Figure 2(a), the chip has six waveguide inputs, with each pair of waveguides representing an element of the unary basis and the state of the ancilla qubit. The chip is divided into distribution loading, payoff calculation, and multiple iterations of quantum amplitude estimation. Figure 2(b) shows the comparison between the theoretical expected payoff and experimental measured payoff during the stepwise iteration of quantum amplitude estimation. In Figure 2(c), the dashed line represents the theoretical expected payoff, the solid line with data points represents the experimental results, and the shaded area indicates the standard deviation (STD) from 50 measurements in each amplitude estimation step. The change in iteration number from 0 to 50 shows the convergence of STD, where represents classical sampling for payoff calculation. Similarly, Figure 2(d) shows the convergence of payoff prediction error as the number of amplitude estimation runs increases. Compared to classical Monte Carlo methods, the unary option pricing method with quantum amplitude amplification achieves a speedup from .png) to

to .png) .

.

Figure 2 (a) Schematic illustration of the photonic computing process. Module is iteratively executed for times. (b) Comparison between the theoretical expected value and experimental results of option payoff calculations, represented in angles. (c) As the iteration number of the amplitude estimation module increases, the standard deviation (STD) of the expected payoff gradually converges, decreasing from an initial value of approximately 0.2 to less than 0.004. (d) With an increase in the iteration number of the amplitude estimation module, the payoff estimation error demonstrates a faster convergence rate compared to classical Monte Carlo methods.

The research team said, "This study, by integrating quantum amplitude amplification algorithms and photonic computing chip technology, offers a rapid and accurate method for option pricing, providing the financial industry with new computational tools, and opening up new prospects for the commercial application of photonic computing technology."