Qiang ZHOU, Ze HE, Yu YANG. Energy geopolitics in Central Asia: China’s involvement and responses[J]. Journal of Geographical Sciences, 2020, 30(11): 1871

- Journal of Geographical Sciences

- Vol. 30, Issue 11, 1871 (2020)

Abstract

Keywords

1 Introduction

Central Asia is at the heart of Eurasia and comprises the former Soviet republics of Kazakhstan, Kyrgyzstan, Tajikistan, Turkmenistan, and Uzbekistan. This region boasts rich energy reserves and so occupies a key geostrategic position globally. The British Petroleum Corporation’s

Thus, as a result of its unique geographic location and abundant energy reserves, Central Asia has become increasingly important in recent years in global oil and gas resource supply and demand and energy geopolitics. The oil and gas refining capacity of Central Asian countries remains generally low, however; compared with abundant known reserves and steadily increasing production capacity, consumption in Central Asian countries also remains relatively low and most production is exported. Before the disintegration of the Soviet Union in 1991, the oil supply capacity of Central Asia remained stable between approximately 50 million tons and 60 million tons. However, since 2000, oil and gas production has continued to rise with the assistance of multinational companies. The difference between production and sales exceeded 100 million tons (i.e., 109 million tons) in 2005 and has continued to grow in a relatively stable fashion. The difference between production and sales in 2016 was 122 million tons. This means that, without taking into account oil and gas production increases in the Central Asia-Caspian region, this former region alone could supply around 120 million tons of oil and gas annually over the next 20 years. Central Asia, therefore, occupies a very important position within the global oil and gas supply market. While Central Asia has physical possession of oil and gas reserves, it does not possess the capital and the technology that would allow it to go into production alone, a fact which brings in the countries and foreign companies with a share in production and revenues. Therefore, one important geopolitical consequence of the demise of the Soviet Union was the rise of intense political and commercial competition for control of the vast energy resources of the newly independent and vulnerable states of Central Asia (

The potential geopolitical implications on the competition for energy resources are complex. From the regional perspective, in addition to Russia and the United States, other major powers such as China, European Union (EU), Turkey, and India have all exhibited different levels of power, interests, and security demands within Central Asia. Mutual competition and coordination have shaped the evolution of geopolitics in this region; the ‘great powers’ (including the United States, Russia, and the United Kingdom) have carried out fierce geopolitical games across Central Asia. The essence of this newly regenerated geopolitical game for energy is twofold: first, control of the production of the oil and gas, and second, control of the pipelines which will transfer the oil to the western markets (

At present, China is facing an increasingly severe international energy situation with rapid economic growth and increasing urbanization level. Central Asia is an important strategic area of China to carry out future international energy cooperation to diversify import oil & gas and enhance energy transport safety (

The aim of this paper is therefore to 1) characterize the energy geopolitical strategies of Russia, the United States, China, and other related powers in Central Asia; 2) analyze the geopolitical and country risks faced by energy cooperation between China and Central Asian countries, and investigate the consequences that such risks could pose to energy cooperation, and; 3) develop a series of policy frameworks that can be used to fortify the stability of the energy cooperation between China and Central Asia and ensure that it can respond flexibly to the array of risks that might be encountered in the coming years.

2 Methodology and data

2.1 Framework

The geopolitical attributes of energy and the geopolitical situation in Central Asia determine that Central Asia’s energy development and cooperation are disturbed by domestic and foreign factors, and face the risk of complex energy structure evolution and geopolitical games, which create a unique energy geopolitical pattern in Central Asia.

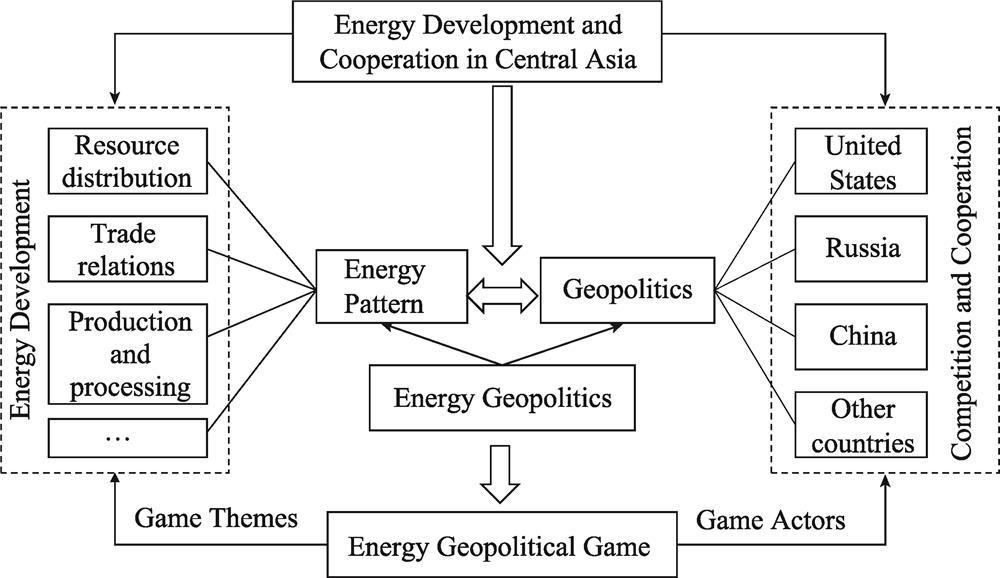

On the one hand, the study of energy geopolitics in Central Asia must take full account of the main actors in energy development in Central Asia. The pluralistic competition led by major powers is the key force in shaping the energy landscape in Central Asia. The great powers such as the United States, Russia, and China are the main countries in the geopolitical game in Central Asia. The EU, Iran, Turkey, Japan, South Korea, and India are also involved in Central Asian energy cooperation in different channels and ways. The above- mentioned countries are the main actors of competition and cooperation in the energy geopolitics of Central Asia. On the other hand, from the perspective of the whole-industry- chain of energy development, resource distribution, trade relations, production, and processing systems are areas among which countries compete and cooperate in Central Asia, thus forming the core themes of competition and cooperation in the energy geopolitics of Central Asia. Actors compete and cooperate around these themes, resulting in complex regional geopolitical relations and the international energy geopolitical game. The framework for the geopolitical analysis of energy in Central Asia is shown in

![]()

Figure 1.

In addition to the geopolitical risks mentioned above, country risks in the political, social, legal, and economic spheres within the Central Asian countries cannot be ignored, as Central Asia is undergoing a period of change in its political and economic transformation. Therefore, China’s energy cooperation with Central Asia must take into account geopolitical and country risks, and develop a series of policy frameworks to promote harmonious coexistence with stakeholders.

2.2 Method and data

Based on the framework of energy geopolitical analysis in Central Asia, this paper mainly adopts qualitative research methods such as historical analysis method and literature method, to focus on analyzing the strategies and specific measures of major countries to participate in the Central Asian energy game and their attitudes towards China and to identify the current main country risks of China’s energy cooperation with Central Asia. At the same time, this paper draws on the oil and gas import and export data from United Nations Conference on Trade and Development (UNCTAD), and data from BP Statistical Review of World Energy, American Heritage Foundation, Transparency International, and other research institutions to support the view.

3 The regional perspective: the current energy geopolitics and the geopolitical risks

The geopolitical entity of Central Asia attracted immediate attention following the break-up of the Soviet Union in 1991. The important geographic location and abundant oil and gas resources of this region quickly meant that Central Asia became the subject of fierce competition between the major global political forces and international capital. Various political forces have launched a sharp and complex contest around energy resource development and the oil and gas pipelines that cross Central Asia. Incomplete statistics reveal that oil companies from the United States, the United Kingdom, France, Germany, Italy, Turkey, Canada, Japan, India, South Korea, Russia, China, Argentina, Hungary, Oman, and the United Arab Emirates have all developed presence in Central Asia for oil exploration and development, crude oil refining, sales, and other activities. Understandably, not all the above-listed countries claim significance in both geopolitics and energy supply. Multi-level competition and cooperation over energy led by the ‘great powers’ quickly became a key force shaping the geopolitical orders in Central Asia. The ‘game’ between China, Russia, and the United States in Central Asia became the dominant force changing the energy geopolitical order of this region and has determined the evolution of the international energy cooperation landscape. The EU, Japan, Iran, India, and Turkey all participate in Central Asian affairs through different channels and means and attempt, to influence energy cooperation developmental trends in this region to achieve their respective strategic goals.

3.1 Russia: a traditional leader of the Central Asian energy geopolitical order

Historically, the persistence of the Soviet Union’s influence over Central Asia’s energy sector led to the majority of the oil and gas flow north to Russia, and from there onward to the industrialized consumer countries of Western Europe (Hart, 2016). In fact, having somewhat recovered from the Soviet collapse, Russia has started to revive its traditional influence on the Central Asian energy sector. Indeed, Russia controls most oil export routes from reserves in Central Asia and around the Caspian Sea. Until 1997, within the energy transportation infrastructure inherited from Soviet times, Russian pipeline networks provided the sole way for land-locked Central Asian exporters to reach external markets and under the monopolistic control of Gazprom. Kazakhstan has maintained stable export-import relations with Russia in the energy sector with no significant changes in the past two decades, and roughly 85% of its oil exports (or some 80 million tons) goes to Europe, mostly via pipelines passing through Russian territory (

| Countries | 2014 | 2015 | 2016 | 2017 | 2018 |

|---|---|---|---|---|---|

| For supplies to Europe | |||||

| Turkmenistan | 11.0 | 3.1 | - | - | - |

| Uzbekistan | 3.6 | 3.5 | 4.3 | 5.5 | 3.8 |

| Kazakhstan | 10.9 | 12.6 | 12.7 | 13.8 | 12.3 |

| For supplies to southern Kazakhstan | |||||

| Uzbekistan | 3.7 | 2.9 | 1.9 | 1.7 | 2.9 |

| For supplies to Kyrgyzstan | |||||

| Uzbekistan | 0.04 | 0.0* | 0.0* | 0.0* | 0.0* |

| Kazakhstan | 0.06 | 0.2 | 0.2 | 0.3 | 0.3 |

Table 1.

Gas purchases in Central Asia by Gazprom Group (billion cubic meters)

Russian policy has focused strategically on the Central Asian energy economic community and integration to build an institutional platform for cooperation and to strengthen its strategic interests. The Russian-led Eurasian Economic Union (EEU) was formally established in 2015 and an Advisory Committee for Oil and Gas comprised of the national energy sectors of member states was created to assess and coordinate policies. This committee approved the ‘Concept for Development of the Common Gas Market of the EEU’ and the ‘Program of Establishing Single Market Space for Oil and Petroleum Products’ and other documents for strengthening regional energy cooperation across Central Asia.

Similarly, Russia has signed a 25-year gas supply agreement with Turkmenistan, 25-year oil cooperation agreements with Kyrgyzstan and Tajikistan, and influences all aspects of energy from production to sales in Kyrgyzstan and Tajikistan. Russia boasts extensive bilateral energy cooperation with all Central Asian countries, including the joint exploration and development of oil and gas resources, the promotion of bilateral natural gas trading, improvements to oil and gas transportation pipelines and other infrastructure, and the promotion of joint research and development on resource exploration and development technologies. The comprehensive ‘double control’ of resources, pipelines, and processing exerted by Russia in this region influences the international energy strategies of Central Asian countries.

In terms of pragmatic cooperation with Central Asian countries, it is clear that Russia possesses incomparable advantages in terms of the history, extent, and scale of energy cooperation. Indeed, given the power of large-scale energy companies, Russia has dominated the cooperation process across Central Asia and has penetrated all aspects of the energy industrial chain. In terms of exploration and the development of the upstream sector, the Russian company Rosneft and the Kazakh company KazMunayGaz signed a contract for the joint development of the Kurmangazy oil field for 55 years in the Kazakh sector of the Caspian Sea (

It is clear that from the Russian perspective, Central Asia is a region with special geostrategic significance. Russia, therefore, acts to strongly exclude any foreign political and economic forces from entering the region. Oil and gas resources in Central Asia are not only an important political and economic lever for Russia to influence these countries but are also an important guarantee that maintains the Russian strategic position in the international energy market. To resist the expansion of the United States power in Central Asia, Russian President Vladimir Putin proposed the creation of an energy club in June 2006 within the Shanghai Cooperation Organization (SCO). At the same time, however, Russia relies increasingly on the Eurasian Economic Community (EAEC) to promote economic integration across the Commonwealth of Independent States (CIS) region. Russia does not want the SCO to decentralize and weaken energy cooperation between Russia and Central Asian countries within the EAEC, so this former organization has yet to establish a multilateral energy cooperation framework and mechanisms widely accepted by member states. At the same time, China has been a pioneer of energy export diversification across Central Asia and so the two countries experience contradictions on this issue. In tandem with Chinese concerns, Russia is also very sensitive to oil and gas cooperation projects in Central Asian countries; for example, after Kazakhstan and Turkmenistan signed an agreement with China to build oil and gas pipelines, Russia signed agreements with Kazakhstan, Uzbekistan, and Turkmenistan to rebuild and build the same kinds of structures, to expand the capacity of the Central Asia- Centre (CAC) gas pipeline network. Russia also proposed to purchase natural gas from Turkmenistan and Uzbekistan at ‘European prices’ to seize and contain Chinese sources. Finally, Russia has encouraged India to enter the Central Asian energy market to balance and reduce the impact of China in Central Asia.

3.2 The United States: power projection in Central Asia to strengthen its control of the global energy market

The interests of the United States in Central Asia can be summarized as security, energy, and democracy (

In terms of strategic layout, United States energy deployment in Central Asia has undergone a transition from a short-term plan to a long-term strategy. It has therefore expanded from emphasis on countries to the surrounding area and from a purely energy economic interest to geostrategic considerations (

In terms of pragmatic energy cooperation, the United States has actively built a bilateral cooperation platform to support the American oil companies that conduct business in Central Asia through a variety of military and diplomatic means. In 1994, the United States government announced a strategy of promoting international investment and trade in Central Asia. In order to control oil from the Caspian Sea in Central Asia, American multinational oil companies became deeply involved in exploration and development at the instigation of their government. Thus, in 1997, the United States and Kazakhstan signed an oil exploration and development contract worth USD 26 billion, and in 2001, American oil companies including Exxon-Mobil, Chevron-Texaco, and their international partners invested around USD 30 billion in energy infrastructure construction in Central Asia. The American International Petroleum Corporation also acquired a range of oil and gas rights in Central Asia and across the Caspian Sea in the form of equity cooperation and joint development. The United States government has proposed 40 specific infrastructure projects since 2011 under their new Silk Road strategic framework to strengthen energy control in Central Asia.

Curbing economic and trade investment and international energy cooperation between China and Central Asian countries is one of the key ways in which the United States can prevent further Chinese expansion and influence in this region. Many American scholars argue that cooperation between the United States and Central Asia should be ‘strong, direct, and long-term’; these workers believe that the United States needs to supplement its ‘Pivot to the Pacific’ through another ‘Pivot to Eurasia’ to curb the rise of China and to ensure that the global economic and security architecture evolves in line with their interests (

3.3 China: an important emerging force in Central Asian energy cooperation

With steady economic growth, China has quickly risen to the top ranks in global energy demand over the past few years. China has become the world’s largest energy consumer, accounting for 23.6% of the world’s primary energy consumption in 2018 (

![]()

Figure 2.

The emergence of China as the important actor in the Central Asian energy sector has profound geopolitical and geoeconomic consequences. Indeed, prior to Central Asia’s opening to China, this landlocked region had just one outlet for its energy exports, through the Soviet-era pipeline network into Russia. Differences in energy endowments mean that China’s imports from Central Asian countries are not the same with natural gas accounting for a high proportion. Central Asian natural gas imports in 2015 accounted for 87.36% of the country’s total imports, while oil imports accounted for less than 1.5% of its total. Natural gas is mainly imported from Kazakhstan, Turkmenistan, and Uzbekistan, while oil imports come mainly from Kazakhstan. In terms of the oil trade relationship with Central Asia in 2005 and 2015 (

![]()

Figure 3.

![]()

Figure 4.

![]()

Figure 5.

Indeed, Kazakh dependence on China’s oil exports exceeded 10% between 2010 and 2013 while China’s dependence on Kazakh oil has always remained below 5%.

Oil and gas cooperation between China and Central Asian countries have diversified over time. The scale of this cooperation has continuously expanded and its degree has deepened, gradually expanding from trade in oil and gas resources to exploration and development, pipeline transportation, oil refining and sales. China has created a complete business chain in the upper, middle, and lower reaches of energy development in Central Asia, including engineering and technical services, and has now further expanded to other related construction areas. Supplies of oil and gas are mainly founded on pipeline transportation, supplemented by road and rail. In terms of diversity and depth of cooperation, China and Kazakhstan have enjoyed the longest time of energy cooperation. Indeed, China has the largest proportion of exploration and development rights as well as export engineering technology services within Kazakhstan with Turkmenistan a close second. In addition to natural gas pipeline construction, China has strengthened cooperation with Turkmenistan in technology services. China’s oil and gas technology services in Uzbekistan have also evolved from petroleum equipment spare part exports to the provision of geophysical exploration, drilling, and logging into upgrading oil and gas engineering technologies and recovery.

The gap in Chinese oil and gas resources is expanding, and so it is necessary to constantly search and identify new supply channels. Energy imports into China are mainly dependent on shipping with 80% of total oil imports transported through the Straits of Malacca. Thus, strengthening oil trade with Central Asia will also improve the safety of international energy transportation channels and reduce the risks and costs. Kazakhstan is key at the moment to China-Central Asian energy cooperation, but relationships with Turkmenistan and Uzbekistan are also growing. Turkmenistan is the most important natural gas importer for China while Kazakhstan remains an important oil importer. Strengthening oil and gas trade cooperation with Central Asian countries is therefore an important strategy to ensure Chinese energy security. Advancements in the Belt and Road Initiative (BRI) mean that interconnections between railways, highways, aviation, telecommunications, power grids, and energy pipelines across China and into Central Asian countries will be greatly enhanced. Energy cooperation between China and Central Asia will therefore be all-round, large-scale, and high-level and developments in core areas of oil and gas resource exploration, development, and production will also deepen.

3.4 Other countries: important balancing forces between Russia, the United States, and China

In addition to the three dominant political forces of Russia, the United States, and China, other external players including the European Union, Japan, India, Iran, and Turkey have also actively participated in energy development in Central Asia because of their own geopolitical and resource strategic considerations. These regional powers are important actors that balance the United States, Russia, and China for Central Asian countries. It is clear that the foreign policy agendas of Central Asian states are likely to become more crowded with the entry of a new actor that is likely to displace or fill, the void left by some of the actors presently engaged in the region (

3.4.1 EU

As the world’s second-largest energy consumer, China is in direct competition with the European Union and experiences a number of contradictions in terms of energy access and transportation pipelines. A report by the European Commission, which dubbed China ‘an economic competitor’ and a ‘systemic rival’ noted China’s ambitions to become a leading global power (

3.4.2 Japan

Japan is also extremely short of energy. As diplomatic relations with Central Asian countries were initiated, the Japanese Mitsubishi Corporation and International Petroleum Exploitation Corporation (INPEX) inspected and conducted energy exploration, exploitation, and transportation in Central Asia. These entities actively sought opportunities for investment in the region. Subsequent to the 1990s, Japan proposed a new strategy of Silk Road diplomacy aimed at enhancing political mutual trust and oil and gas resource cooperation with Central Asian countries. Recently, cooperation on energy such as on nuclear energy and nuclear related issues, strengthening transportation infrastructures, aid programs and conducting periodic diplomatic talks are main pillars of Japan-Central Asian countries relations (

Japan also competes with China in terms of energy cooperation in Central Asia. Due to the complicated rivalry over war history and territorial claims between China, Japan and Korea, it is therefore difficult for Japan to carry out cross-border energy cooperation with Central Asia in Northeast Asia. To find a breakthrough, Japan has actively assisted Central Asian countries to build a ‘southern route’ from Afghanistan to the Indian Ocean in order to bypass long-distance cross-border transport through China and Northeast Asia. Thus, in 2004, Japan launched the bilateral dialogue mechanism ‘Japan + Central Asia’ in order to restrict the SCO and balance the influence of China and Russia in the region. In 2006, the Foreign Ministers’ Meeting of ‘Japan + Central Asia’ adopted a plan of action for energy cooperation, investing in the construction of highways and oil and gas pipelines connecting Tajikistan and Afghanistan and transporting oil and gas from Central Asia to Japan through the Indian Ocean sea passage. Japan has also long been concerned about the SCO developing into an exclusive regional group dominated by China and Russia in the hinterland of Eurasia. Japanese participation in Central Asian energy competition is therefore not just to obtain resources but also to increase the cost of Chinese imports by influencing price fluctuations and pipeline construction.

3.4.3 India

India is always aware of the enormous energy reserves within its geographically proximate Central Asian region that could potentially fulfil its energy demands (

3.4.4 Iran

Iran is superbly located both geographically and strategically. The country not only has the possibility of the shortest connections to traditional and emerging energy markets but can also become an important transport knot for Central Asia’s gas stream (

3.4.5 Turkey

One equally important actor on the Caspian energy transport corridor is Turkey. For BTC, the role of Turkey as an indispensable transit country is most obvious. Turkey also takes advantage of the current favorable opportunity to ‘de-Russia’ among Central Asian countries. This nation has therefore also developed all-round cooperative relations with Central Asia and strives to play the role of regional power. In terms of energy, Turkey needs to acquire oil and gas resources from Central Asia but also strives to build an energy transmission hub connecting Europe and Asia. Thus, with the support of western countries, Turkey actively promotes the energy strategy referred to as the ‘East-West Energy Corridor’. In light of the current containment and isolation of Iran, most newly built pipelines of the United States and European Union across Central Asia pass through Turkey, including the BTC and BTE pipelines, the under construction Trans-Anatolian Natural Gas Pipeline (TANAP), the trans-Adriatic pipeline (TAP), and the aborted Nabucco Natural Gas Pipeline. Turkey reached a framework agreement with Turkmenistan in 2014 regarding the construction of a Caspian Sea pipeline and the entry of natural gas into Europe that will strengthen its position as an energy hub. Turkey also does not want China to become the dominant energy force in Central Asia and competes with China in many areas. Future conflicts between China and Turkey are likely in the context of Central Asian oil and gas supplies.

3.5 Development of an energy geopolitical order in Central Asia

It is certainly the case that multi-party competition is a new feature of the energy geopolitical order in Central Asia. Struggles and coordination among energy exporters, importers, and transit countries have exerted a profound impact on the energy order of Central Asia (

China, Russia, and the United States are the three most influential powers in Central Asia. In recent years, all the three have proposed strategic ideas for this region. Following the global financial crisis in 2008, both the United States and Russia accelerated adjustments to their strategies in Central Asia and competed for energy geopolitical dominance. The United States put forward the ‘New Silk Road’ initiative in 2011 which aimed to create a new international strategic passage through Central Asia into South Asia with Afghanistan at its core. Simultaneously, Russia issued a report entitled ‘A new integration project for Eurasia: The future in the making’ which explicitly proposed the establishment of a ‘Eurasian Union’ within the area of the former Soviet Union for the first time. China then proposed the BRI in the autumn of 2013 and via the subsequent release of the ‘Vision and Action to Promote the Construction of the Silk Road Economic Belt and the Maritime Silk Road in the Twenty-first Century’. Unlike the West, China makes no demands for political reform from Central Asian governments. Unlike Russia, China does not use political pressure to keep the region in its general orientation (

Although the geopolitical imagination of large powerful countries acting in Central Asia has contributed to the integration of this region into the global economy, these forces have also led to destructive competition between the United States, China, and Russia. A number of authors (e.g.,

4 Country levels: the country risks caused by internal changes in Central Asia

The complexity of the geopolitical environment within Central Asia is not just reflected in the competition and cooperation between the big powers but also in Central Asian countries confronting by complex challenges including international terrorism, religious extremism, illegal drug trafficking, transnational water sharing, transnational criminal, boundary issues. In addition, Central Asian countries are entering a critical phase of internal change, uncertainties in the development of different countries such as democratic transformations, economic reforms, domestic governance, and other external factors such as the new ‘great game’. The country risks faced by Central Asian countries include complexity, comprehensiveness, and linkage, mainly manifested in political and cooperation systems, legal policies, and treaty agreements.

4.1 International energy cooperation in Central Asia is significantly influenced by political systems

Central Asia comprises five culturally and ethnically diverse countries that have taken different paths in terms of political and economic transformation over the nearly 30 years since their independence from the Soviet Union. The development of these five countries has been extremely unbalanced, characterized by territorial differences and the lack of a platform for cooperation in regional affairs. In terms of security, the situation in most parts of Central Asia remains relatively stable even though it is undeniable that the hidden danger of religious extremism still exists. Kazakhstan boasts the best security environment while the situation in the three countries bordering Afghanistan (Uzbekistan, Tajikistan, and Turkmenistan) is more serious, especially in Tajikistan. In terms of the economic environment, almost all countries have failed to achieve significant success in building a competitive, diversified, and open economy. High dependence on oil and gas industries means that Central Asian countries have implemented highly monopolized resource development policies. The international energy policies of Central Asian countries are therefore based more on political considerations than purely commercial behavior; this situation means that serious corruption can occur easily alongside power rent-seeking and economic crimes. Resource cooperation processes are also seriously affected by these political systems. One report published in 2018 by the American Heritage Foundation’s Economic Freedom Index (

![]()

Figure 6.

![]()

Figure 7.

4.2 International cooperation systems for Central Asian energy lack integrity and are non-systematic

Although a multi-level and multi-field energy cooperation system is present in Central Asia, complexity and fragmentation are obvious. The international energy cooperation system in Central Asia presently encompasses three facets. The first of these is the energy cooperation system coordinated by international organizations, including multilateral mechanisms under the framework of cooperation including the Central Asia Regional Economic Cooperation (CAREC) Program led by ADB. The second main system comprises bilateral energy cooperation and dominated by big powers outside of Central Asia, including within the BRI framework, under the ‘New Silk Road’ strategy of the United States, and under Russian energy strategy

2035. The third system in place comprises multilateral cooperation within the EEC framework and Trans-Caspian oil and gas cooperation. An increase in ‘institutional density’ within Central Asia has led to an inter-relationship phenomenon and even conflict between these systems. Amongst the numerous energy cooperation systems, no single dominant approach has received widespread support from all parties, a factor which creates numerous uncertainties for future energy cooperation prospects. The five Central Asian countries, together with the three leading powers (China, the United States, and Russia) and other countries such as the European Union, Japan, South Korea, India, Iran, and Turkey have also reached energy cooperation agreements and formed exclusive energy cooperation blocks. Numerous countries also participate in this region via international oil companies as main actors. This means that the positions and identities of Central Asian countries in cooperation with other nations and international oil companies are split. The diversification of power and system decentralization will inevitably lead to an energy cooperation dilemma in Central Asia.

4.3 Lack of consistency in international energy investment laws and policies

Central Asian countries are generally short of funds and technology. This means that providing preferential conditions for cooperation and attracting foreign investment have become important ways to develop the energy economies in this region. Central Asian countries have formulated and promulgated a series of laws and regulations for the oil and gas industry to stimulate development. Kazakhstan, for example, has enacted the Petroleum Law, The Subsoil Code, the Foreign Investment Law, and the Code ‘On Subsoil and Subsoil Use’ (SSU Code, 2017), while Turkmenistan and Uzbekistan have enacted the Foreign Investment Law of Turkmenistan and the Foreign Investment Law of the Republic of Uzbekistan, respectively, and have initially established relatively complete legal systems just for energy investment.

The laws and policies of Central Asian countries remain inconsistent, however, and are influenced by the government; this means that the risk of legal changes remains relatively high. Central Asian countries have also made arbitrary amendments to existing legislation by signing policy documents like presidential decrees; these actions also reduce the binding force and credibility of laws and increase the legal risks of foreign oil and gas resource investments being taxed.

It is particularly noteworthy that from the 21st century on, influenced by the worldwide nationalization of energy production, Central Asian countries have more frequently amended and supplemented laws and regulations that apply to the oil and gas industry, strengthened the control and supervision of this sector, and replaced mild and relaxed foreign investment environments and fiscal and taxation policies with mandatory ones. In Kazakhstan, for example, a new tax policy was introduced in 2009 to dramatically adjust the collection methods for oil and natural gas exploitation, new mineral resource exploitation and oil and gas export revenue taxes were levied, and the calculation protocol for excess profits was modified. Kazakhstan has also revised its code ‘On Subsoil and Subsoil Use’ many times, expanding control over its own resources and strengthening its supervision over previous oil and gas contracts. Government intervention, legal changes, tightening policies, and other factors have become important risks for international energy investment in Central Asia.

4.4 Ambiguous energy cooperation treaties and agreements between China and Central Asia

Two forms of energy investment treaties and agreements have been adopted by China in Central Asia. The first of these are international treaties and regional agreements. The Washington Convention of 1966 and the Seoul Convention of 1985 are still the main sources of law that apply for the settlement of international disputes in Central Asia. China, Kazakhstan, Tajikistan, Kyrgyzstan, and Uzbekistan all joined the SCO in 2001 (to the exclusion of Turkmenistan) to establish and expand cooperation frameworks in political, economic, and energy fields. Energy-related agreements within the ‘Action Plan on Implementation of the Programme of Multilateral Trade and Economic Cooperation of SCO Member States’ have provided important legal foundations for countries in the region to engage in energy cooperation and investment. Most of the contents involved are nevertheless just principled or framework provisions, and the multilateral energy cooperation mechanism remains imperfect. The second group of agreements is mainly based on bilateral investment treaties (BITs) which themselves contain different degrees of legal status provisions with respect to ownership and international investment dispute settlement mechanisms alongside vague provisions on matters related to energy investment. Indeed, only China and Uzbekistan re-signed the BIT in 2011, which means that agreements with other countries were signed in 1992 or 1993. The political situation, economic environment, and investment behavior of bilateral agreements have also changed significantly over the last two decades. Compared with bilateral agreements signed between China and developed countries, those with Central Asian counterparts tend to be simple in content, lack clear and operable provisions in several important areas, and can no longer be adapted to current investment. This means that Central Asian countries are relatively weak overall from the perspective of bilateral agreements. These agreements therefore tend to be significantly influenced by international politics, military affairs, economic development, and international trade, and are sensitive to external environmental changes. Agreements signed with China therefore tend to have marked conservative tendencies.

5 Comprehensive strategies for energy cooperation to meet geopolitical and country risks between China and Central Asia

The energy cooperation between China and Central Asia is based on the common interests of both sides, and is also based on the complementary energy endowment and energy market of both sides. As implementation of the BRI has accelerated, the scale and breadth of investment and personnel flow between China and Central Asia will be greatly enhanced and interactions between the two regions will become more frequent and ever closer. The overall security situation in Central Asia may also become more severe which will also increase the security risks to overseas interests. In order to build a risk prevention mechanism for energy cooperation between China and Central Asia, the former should not only consider the ‘great game’ amongst big powers but should pay attention to the country risks within Central Asian countries. In view of the potential geopolitical game played by the big powers as well as rising country risks within Central Asian countries, comprehensive strategies are proposed so that China minimizes the risks of energy cooperation.

5.1 Establishing energy cooperation partnership with great powers

To effectively cope with the geopolitical risks and national risks of energy cooperation in Central Asia, there is a clear need for cooperation among major powers. Although the complex interactions between China, the United States, and Russia in Central Asia have intensified the fragmentation of the security landscape in the region, there are still some ways to alleviate the zero-sum competition among major powers. The great powers have more to gain from cooperation than outright competition. In order to reduce the doubts and counter-measures caused by other big powers on China’s excessive growth in Central Asia, China must coordinate its energy cooperation with other major powers in Central Asia. Throughout the process of promoting energy cooperation with Central Asia, China should fully consider the energy interests and economic penetration of Russia, the United States, and other major countries in Central Asia. This will enable China to formulate a multilateral cooperation framework involving different stakeholders including energy exporters, transit countries, and importers, as well as form a community of energy destiny that safeguards common interests.

5.2 Promoting the establishment of a pragmatic and efficient multilateral energy

cooperation mechanism

Traditional experience shows that building a pragmatic and efficient regional multilateral energy cooperation mechanism can effectively safeguard regional energy security and bring collective benefits to participants. The bulk of relevant international energy cooperation frameworks and agreements in Central Asia are currently principled but there is still no substantive framework for energy cooperation. The priority here is to strengthen government-led multilateral energy conversation mechanisms. Thus, taking into account the current energy situation in China, difficulties in bilateral cooperation, and the complex energy geopolitics of Central Asia, it will be necessary to strengthen Chinese capacity for multilateral energy dialogue from a strategic perspective. China could also coordinate the energy agencies of China, Kazakhstan, Turkmenistan, Uzbekistan, Kyrgyzstan, and Tajikistan to establish a multilateral energy dialogue mechanism specifically for Central Asia. The countries that participate in such a multilateral energy dialogue should share their energy information and deepen political trust to ensure the practicability and stability of multilateral cooperation. China should also strengthen SCO energy cooperative consultation under the auspices of the BRI and create a multilateral energy cooperation mechanism that has both practical significance and binding force.

5.3 Promoting the diversification of energy cooperation entities

Optimizing the corporate structure of energy cooperation across Central Asia is another key measure that must be taken. China presently participates in the energy affairs of Central Asian countries via state-owned energy enterprises. Energy as a strategic resource and thus the overseas economic activities of state-owned enterprises are usually labeled as state behavior, a categorization which will cause concern for the governments and people of Central Asian. At the same time, the shortcomings of the state-owned enterprise system, long-term decision-making processes, and a lack of flexibility will weaken the competitiveness of Chinese energy companies in the context of overseas cooperation. In order to consolidate existing energy cooperation platforms established by state-owned enterprises, China should actively encourage small- and medium-sized energy enterprises to participate in Central Asia. This will strengthen the cooperation between state-owned enterprises and private enterprises, establish ‘going out’ industrial alliances, and form strategic relationships with Central Asian national petroleum companies. These activities will also enable the avoidance of all kinds of natural and human risks caused by insufficient access to energy resources in local economic and social environments.

5.4 Innovating the cooperation models of energy projects

The operating model for energy cooperation projects between China and Central Asia can also be innovated. China can give full scope to the advantages of exploration technology and strengthen technical trade services in this sector alongside the development of oil and gas fields as well as the construction and maintenance of infrastructure, and ‘turnkey projects’ for product processing. China should also sign similar technical assistance programs or technology trade service contracts with Central Asian countries to help them improve their energy industrial chain technologies at the right time. This will fundamentally promote the modernization of the energy sector in Central Asian countries. Finally, China can also enhance the depth and breadth of cooperation with Central Asian countries in production services industries such as logistics, trade, finance, labor export, and management.

5.5 Exploring a co-construction zone and establishing a joint reserve mechanism

Exploring the establishment of a cross-regional energy joint reserve mechanism is also concordant with the long-term energy strategy development needs of China and Central Asian countries. This is also an important component of Chinese and Central Asian needs to deepen energy security. Thus, building a transnational energy reserve mechanism will also be conducive to stabilizing the long-term energy supply of a host country, reducing the impact of wars, extreme events, and changes in the international political situation. This process will also help supply countries to avoid the impact of price fluctuations in the energy market and ensure long-term oil and gas income. Cross-regional energy joint reserves are not limited to bilateral cooperation; however, China can implement joint energy reserves with Kazakhstan, Turkmenistan, and Uzbekistan to start with in Central Asia. It should also be possible to coordinate the transnational reserves of these three countries at the same time to maximize the energy income of Central Asian countries and ensure a stable supply for China.

5.6 Establishing energy advisory service institutions and information platforms

The creation of a professional energy advisory service organization and an energy information platform that draws in wide participation is also urgent problems for Central Asia. It is necessary to set up a semi-independent energy consulting organization composed of experts from various fields including energy technology, strategy, economics, law, enterprise management, and information. This organization should emphasize the professionalism and independence of non-government personnel including experts, scholars, and consultants in decision-making services. A broad and targeted platform for energy cooperation can then be established to rapidly share data, eliminate information asymmetry, save transaction costs, improve the efficiency of energy cooperation, and reduce risks.

6 Conclusions and discussion

International Energy Agency (IEA) predicts, by 2030, continued increases in demand for transport fuels means that China will become the world’s largest oil consumer, taking over from the United States. Import dependence, especially for oil, reaches levels that require annual spending of nearly half a trillion dollars on energy imports by 2040, posing potential risks to energy security. Central Asia has long possessed large volumes of oil and natural gas, which is emerging as an important strategic region for China’s international energy cooperation. Central Asia can alleviate China’s increasingly tight overseas oil and gas resources in terms of energy supply, energy transportation security, and geopolitical security. Deepening energy cooperation with the region is an important strategy for China to diversify overseas oil and gas imports and to ensure energy transportation security. It is important to note that China and Central Asian energy cooperation are strategically complementary and will have broad strategic advantages in the fields of oil trade, oil and gas resources exploration and development, and product processing technology.

The growth of China’s economy at historically unprecedented speed and scale over the last three decades has completely altered the supply-demand equation of global energy (

It should be noted that because of deepening energy cooperation, China and Central Asia will be more closely linked, therefore, risks at regional and national levels are bound to be related to both internal and external linkages. Contemporary Central Asia in the process of transformation and facing considerable political, social, cultural changes challenges,and the resulting country risks require special attention. Although the five Central Asian countries are described as a group of countries in this paper, there are significant differences between these countries, and therefore, China should adopt a differentiated strategy when engaging in energy cooperation with Central Asian countries.

China’s energy cooperation in Central Asia is facing geopolitical risks and country-specific risks. Choosing a reasonable model of cooperation can, to a certain extent, reduce the risks of energy cooperation and maximize the security of energy supply. This paper suggests some models for cooperation between China and Central Asia in energy cooperation, but it is important to note that the models do not exist in isolation from each other and that the choice of models is not absolute. The next step in the study should be to explore how cooperation models or combinations of models can be proposed for different countries and projects to maximize the stability of energy supply and ensure energy security.

References

[1] AminjonovF. Russia’s evolving energy interests in Central Asia and Afghanistan. Bishkek Project(2017).

[2] AndersonJ E, MarcouillerD. Insecurity and the pattern of trade: An empirical investigation. Review of Economics and Statistics, 84, 342-352(2002).

[4] Andrews-SpeedP, LiaoX, DannreutherR. The Strategic Implications of China’s Energy Needs. Routledge(2014).

[5] ArvanitopoulosC. The geopolitics of oil in Central Asia. The Journal of Modern Hellenism, 67-90(1998).

[7] ChowE C, Hendrix, LE. Central Asia’s pipelines: Field of dreams and reality. NBR Special Report, 29-42(2010).

[8] CohenA. US interests and Central Asia energy security. Backgrounder, 1-11(1984).

[12] FarkhodT. Geopolitical stipulation of Central Asian integration. Strategic Analysis, 34, 104-113(2010).

[13] FazilovF, ChenX. China and Central Asia: A significant new energy nexus. The European Financial Review, 38-43(2013).

[15] IslamA. The US role and policy in Central Asia: Energy and beyond. Arts Faculty Journal, 33-51(2010).

[16] KouZ. A new pattern of oil and gas exports in Central Asia. International Petroleum Economics, 18, 39-47(2010).

[17] LenC. China’s 21st Century Maritime Silk Road initiative, energy security and SLOC access. Maritime Affairs: Journal of the National Maritime Foundation of India, 11, 1-18(2015).

[18] LiH Q, WangL M, LangY H. Evolution process and driving mechanism of energy geopolitical pattern: A study of Central Asia. World Regional Studies, 18, 56-65(2009).

[19] LuJ. A new geopolitical pattern in Central Asia and its strategic influence on China. World Regional Studies, 20, 8-14(2011).

[20] MarketosT N. China’s energy geopolitics: The Shanghai Cooperation Organization and Central Asia. Routledge(2008).

[21] MuzalevskyR. China’s rise and reconfiguration of Central Asia’s geopolitics: A case for U.S. “Pivot” to Eurasia. Current Politics & Economics of Northern & Western Asia, 24, 155-162(2015).

[24] PetersenA, BaryschK. Russia, China and the geopolitics of energy in Central Asia. Centre for. European Reform(2011).

[25] PeyrouseS. A donor without influence: The European Union in Central Asia. PONARS Eurasia Policy Memo, 478(2017).

[27] PopI I. China’s energy strategy in Central Asia: Interactions with Russia, India and Japan. Revista UNISCI, 197-220(2010).

[28] RaballandG, KunthA, AutyR. Central Asia’s transport cost burden and its impact on trade. Economic Systems, 29, 1-31(2005).

[29] RakhimovM. Contemporary Central Asia: Balancing between Chinese and Trans-Asian ‘Silk Road’ Diplomacy, China’s Global Rebalancing and the New Silk Road. Singapore: Springer, 119-128(2018).

[30] RumerE B, SokolskyR, StronskiP. US policy toward Central Asia 3.0. Washington, DC: Carnegie Endowment for. International Peace(2016).

[31] SavinV, OuyangC S. Analysis of Post-Soviet Central Asia’s oil & gas pipeline issues. The Journal of Eurasian Affairs, 24-38(2013).

[32] ShiC. Opportunity and challenge exist in participating in the oil and gas resources of Russia for China’s enterprise. China Economic & Trade Herald, 27, 39-40(2010).

[33] StobdanP. India and Central Asia: Untying the energy knot. Strategic Analysis, 40, 14-25(2016).

[34] StronskiP, NgN. Cooperation and competition: Russia and China in Central Asia, the Russian Far East, and the Arctic. Washington: Carnegie Endowment for International Peace(2018).

[35] XuH F, LiY. Analysis on the factors of energy cooperation in power countries in the “Silk Road Economic Belt”. International Forum, 18, 30-36, 78(2016).

[36] XuQ H. New Geopolitics: Energy in Central Asia and China(2007).

[37] XuX, ChengJ, WangY. Energy strategy adjustment of Russia and the cooperation of oil & gas resources between China and Russia. Russian Studies, 27, 54-58(2007).

[39] YangY, LiuY, JingF J. Study on energy cooperation between China and the Central Asia and Russia under the view of energy geopolitics. Geographical Research, 34, 213-224(2015).

[40] YangZ. Situation, defect and improvement of legal system of energy cooperation between China and Central Asia states: Form the Silk Road Economic Belt. Law Science Magazine, 37, 18-28(2016).

[41] ZieglerC E, MenonR. Neomercantilism and great-power energy competition in Central Asia and the Caspian. Strategic Studies Quarterly, 8, 17-41(2014).

Set citation alerts for the article

Please enter your email address

© Copyright 2018-2021 | Chinese Laser Press. All Rights Reserved 沪ICP备15018463号-20